by Scott Emick

8/9/25

updated 8/29/25 – Added the post account closure letters.

1. Introduction

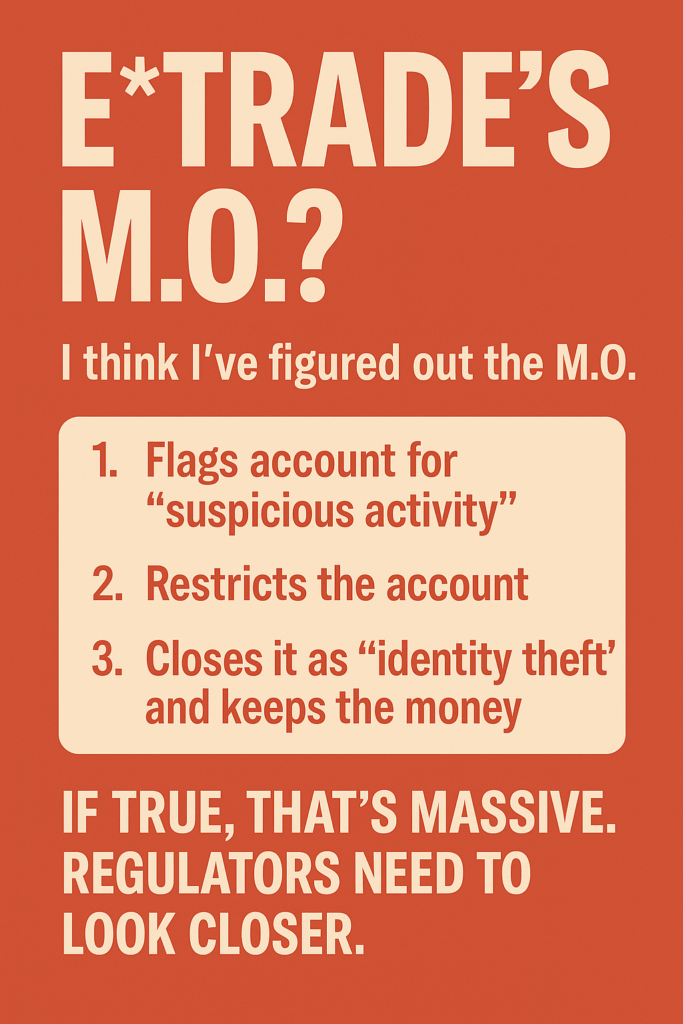

In August 2025, I experienced unexpected account closures and the withholding of both a $55,000 cashier’s check deposit and my existing funds (cash and stocks) at E*TRADE brokerage, about $60,000 USD after I requested to wire Kraken three times. My E*TRADE Checking account which was also open many years was closed. Both Accounts were closed due to what amounts to identity theft.

The closure letters stated the accounts were new and that someone else had used my information to open each one. This closure reason is false as my accounts were open many years and also nobody had used my information to open then other than me. E*TRADE verified my identity at least a dozen times. The use of this reason on account closure letters is deeply troubling after trying to make a wire request to a domestic USD account in my own name.

This article outlines my experience, the steps I took, and the potential legal and regulatory issues I believe may be relevant — so others can understand their rights if they encounter similar issues.

2. My Experience – Timeline of Events

- July 18, 2025: I deposited a $55,000 cashier’s check via the E*TRADE mobile app, carefully selecting my checking account. Despite this, the funds were posted to my brokerage account. I also had approximately $5,000 in cash and stock holdings across my E*TRADE accounts prior to this deposit. I had also deposited a personal check on July 7th, 2025 selecting etrade checking and this was also misposted to my brokerage account.

- Verification Process: After I waited over a week for the cashier to check clear and be available, I put in a wire request to Payward Inc/Kraken on July 28th. E*TRADE removed my access to accounts on the web and app, placed my accounts under review, requiring verification of both the 55K USD check and the previously deposited check from July 7th 2025. This process took about a week because they required the check writers, their banks, E*TRADE, and myself to be on calls together. The issuing banks confirmed the checks had cleared, were not fraudulent, and were not subject to recall. The writers confirmed they were not being scammed and were paying me money owed to me.

- Privacy Concern: Because E*TRADE allegedly could not host a four-way call, I was instructed to connect the check issuers into a three-way call while E*TRADE called their banks. This exposed the check issuers’ account numbers, password hints, and answers to security questions to me — something I did not request and believe should have been avoided to protect their privacy.

- Wire Transfer Request: Once the checks were confirmed, I requested my wire transfer be resumed. I was wiring to a USD account at a state-chartered, FDIC-insured bank in Wyoming (Payward, Inc., parent of Kraken) via an intermediary Dart Bank. When asked if this was a crypto account, I explained it was a USD bank account, not a cryptocurrency address, and that it is not possible to wire directly to a crypto address. Once a USD account is funded with Kraken, it is then possible to trade dollars for bitcoin or other crypto. The wire request details were verified with me and I was told the wire would go out that day. This was on or around August 3rd.

- The wire never went out. I called back on August 4th and was asked some standard compliance questions to make sure I wasn’t being scammed. Darius was very kind with me on the phone and assured me after I answered the questions that everything was in order and the wire would go out.

- Account Closure: The wire was never sent. On August 5, 2025, E*TRADE closed my accounts without even notifying me. I found out again from trying to sign into the app. When I called I was told that E*Trade “No longer wished to do business with me.” and that “My accounts had been closed”. They made no mention of paying me with a check as is most banks standard operating procedure when they close acounts. When I asked when they would issuing me a check, I was told they were not and told me to “recall the funds,” which is not something a consumer can do — especially when no wire was actually sent. No reason for the closure was given. While I cannot say definitively that my intended transfer to a bank associated with a cryptocurrency exchange was the cause, the timing raises concerns about whether such transactions are being flagged or restricted.

- I had deposited the cashier check and initiated the wire while I was at home in Ohio, but followed up while on vacation in California.

- August 7th, 2025. I filed a complaint with the CFPB first asking that my account be reinstated per the Trump Executive Order on debanking.

- Closure Letters(s): I received letters stating my accounts were closed because they were newly opened and that someone else had used my information to open them. Both of these patently false.

- Major Red Flags here. E*TRADE choose the wrong account closing status and keeps my funds!!!

- After some research and finding that E*Trade may have violated criminal laws and probably lied to me (it is impossible for me to recall funds and that is what they told me), I decided maybe its better to just shoot for closing my accounts and receiving funds owed to me. I filed updated complaints with the CFPB and OCC. I sent an email to the Secret Service about a possible criminal referral.

- I plan on contacting my Congressional Representatives and the office of the President of the United States as well.

- I will contact attorneys to see if its feasible to sue E*Trade. I will make posts on social media to draw awareness to my problem and share information with others who have also been targeted.

3. Potential Legal and Regulatory Issues

(Listed as possible violations based on the facts as I understand them. This is not a legal determination.)

Federal Banking Laws

- Regulation CC (12 C.F.R. Part 229) – Timely funds availability after verification, especially for cashier’s checks.

- 18 U.S.C. § 1344 – Bank Fraud – Obtaining or withholding funds under false pretenses.

- 18 U.S.C. § 1343 – Wire Fraud – Misrepresentation in relation to wire transfers.

- 18 U.S.C. § 656 – Theft/Embezzlement by Bank Employee – Misapplication of funds by bank employees.

- 12 U.S.C. § 5531 (Dodd-Frank / UDAAP) – Prohibits unfair, deceptive, or abusive acts or practices.

Federal Privacy Laws

- Gramm-Leach-Bliley Act (15 U.S.C. §§ 6801–6809) – Requirement to protect nonpublic personal information (NPI).

- Regulation P (12 C.F.R. Part 1016) – Privacy rules implementing GLBA.

State Laws – Ohio & California

- Ohio Rev. Code § 2913.02 – Theft

- Ohio Rev. Code § 2913.43 – Securing Writings by Deception

- Ohio Common Law – Conversion – Wrongful exercise of dominion over another’s property, including specifically identifiable funds, in a manner inconsistent with the owner’s rights. (Joyce v. General Motors Corp., 49 Ohio St.3d 93)

Cal. Penal Code § 484 – Theft by Larceny/Fraud - Cal. Bus. & Prof. Code § 17200 – Unfair Competition Law (UCL)

- California Consumer Privacy Act (CCPA) – If applicable, prohibits disclosure of personal information without consent.

4. Why This Matters

For customers, this case highlights the importance of:

- Knowing your rights on funds availability and account closures.

- Understanding how wire transfers to legitimate, regulated financial institutions can still be blocked.

- Being aware of privacy obligations when banks involve customers in verification calls.

5. What To Do If This Happens To You

- Document Everything – Keep copies of checks, bank confirmations, emails, and call logs.

- File Regulatory Complaints – OCC, CFPB, and state attorney general.

- Ask Directly About Holds – Confirm if there’s any seizure order or legal restriction.

- Report Privacy Breaches – If NPI is disclosed without consent, report under GLBA and state privacy laws.

- Consult Legal Counsel – Especially if significant funds are involved.

6. Disclaimer

This article reflects my personal experience and understanding of the events, and identifies laws and regulations that may be relevant. It is not a legal determination of wrongdoing and is provided for informational purposes only.